Biosecurity, trade deals and water storage top KPMG agribusiness priorities

Biosecurity, trade deals and water storage top KPMG agribusiness priorities

Tim McCready

New Zealand’s food and fibre sector could disappear tomorrow and global markets would barely notice.

That was the provocation from one industry leader during this year’s KPMG Agribusiness Agenda roundtable discussions on international markets.

They qualified it: while New Zealand is a relatively small cog in an enormous system, it would absolutely be missed.

Customers do not choose New Zealand because we are the cheapest producer. They choose New Zealand for attributes that are harder to replicate, including its stability, world-class biosecurity, sustainable production systems, adherence to international trade rules, high food safety standards and reputation as an ethical and transparent partner.

Those attributes have earned New Zealand a place in global value chains. The challenge now, as the Agribusiness Agenda outlines, is for the food and fibre sector to build on these strengths while continuously evolving to meet the changing needs of our customers.

New Zealand will never compete by being the biggest producer. New Zealand is a small producer in global terms and geographically distant from almost every customer.

There is consensus among contributors that the peak of globalisation has passed. Governments, rather than markets, are setting the rules for global trade, and geopolitical shifts have become one of the most significant risks exporters now face.

Against that backdrop, several argue that New Zealand’s stability, biosecurity status and reputation for playing by the rules matter as much to buyers as anything coming off the farm.

That conversation sits behind the entire 2026 Agribusiness Agenda.

KPMG challenged contributors with a broad question: whether existing settings remain fit for purpose, or whether more fundamental shifts are required to secure long-term success.

Around three-quarters of contributors favour change over the status quo, noting that current settings and processes may constrain the sector’s potential as it responds to disruption such as climate change and geopolitical shifts.

This doesn’t mean abandoning New Zealand’s strengths. Rather, contributors repeatedly argue for continuous evolution – ensuring products, production systems and business models evolve alongside customer demand instead of relying on historical competitive advantages.

The report identifies 24 “global future shapers” that will reshape food systems over the next quarter century.

They range from geopolitical fragmentation, cyber risk and changing demographics, to AI, water scarcity, climate change and the growing convergence of food and pharmaceuticals.

Others point to the integration of nature into business models – including the rise of the circular bioeconomy – and increasing pressure on ageing infrastructure.

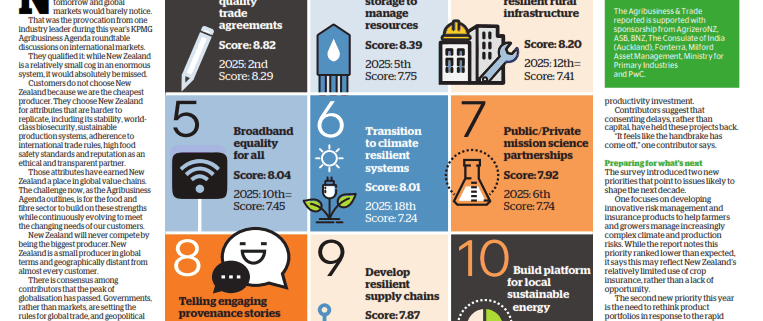

Each year, KPMG asks contributors to score a set of priorities for the organisations they represent in the food and fibre sector. This year, 105 leaders worked through 39 priorities on a scale of 1 to 10, with 10 indicating that the issue is considered a critical priority.

For the 16th consecutive year, world-class biosecurity remains the sector’s highest priority. This year’s score (9.40 out of 10) is the highest score reported for any priority since 2018 – the year Mycoplasma bovis and Myrtle Rust pushed biosecurity to an all-time survey record of 9.62, demonstrating the enormous economic cost of a single biosecurity failure.

The concern now is that future incursions become harder to prevent. Increasing international connectivity and evolving production systems create new pathways for pests and diseases to enter New Zealand.

Contributors point out that many of the country’s most important export sectors are built on monocultures, making a single breach a bigger risk to economic resilience than is often acknowledged – and one that alignment between industry and government is critical to managing.

Signing high-quality trade agreements again ranked second in the survey. Contributors also say that existing agreements need to be actively managed and evolve to remain fit for purpose, and investment is required in regulatory systems and infrastructure to ensure organisations can fully utilise the market access already secured.

Building resilience

Several priorities recorded significant movements in this year’s survey, reflecting how leaders see the sector adapting to a more uncertain future.

Resilient rural infrastructure jumped from 12th-equal last year to fourth place.

Contributors link it directly to operational efficiency – and to the sector’s ability to attract the best talent.

Transition to climate-resilient farming systems rose from 18th last year to sixth, a sharp turnaround for a priority that was ranked lowest of all in 2024.

Building a platform for local sustainable energy climbed into the Top 10 for the first time this year, from 27th in its debut year in 2024, to 12th equal last year, to 10th now.

The rise in water storage as a priority reflects a similar shift. It reached third place – its highest ranking since 2013. Contributors frame water infrastructure as a strategic capability that underpins productivity, social licence and diversification, rather than simply a productivity investment.

Contributors suggest that consenting delays, rather than capital, have held these projects back.

“It feels like the handbrake has come off,” one contributor says.

Preparing for what’s next

The survey introduced two new priorities that point to issues likely to shape the next decade.

One focuses on developing innovative risk management and insurance products to help farmers and growers manage increasingly complex climate and production risks. While the report notes this priority ranked lower than expected, it says this may reflect New Zealand’s relatively limited use of crop insurance, rather than a lack of opportunity.

The second new priority this year is the need to rethink product portfolios in response to the rapid uptake of GLP-1 weight-loss medicines.

This priority ranked 37th with a score of 6.25 – near the bottom of the survey. The report suggests the ranking may understate the significance of the issue.

Around the world, food companies are already reshaping product portfolios as consumer preferences evolve. For New Zealand, the shift may prove more opportunity than threat. Protein sectors broadly are seen as well placed to benefit, with red meat among those already seeing early demand and pricing effects offshore.

Technology, particularly artificial intelligence, sits beneath many of this year’s priorities.

AI is rapidly changing how global consumer packaged goods companies understand consumers, develop products and forecast demand, contributors say. It is no longer a source of competitive advantage in itself. The report describes it as a “ticket to play” – a capability that organisations must have to remain relevant.

That is the thread running through the entire Agribusiness Agenda.

If New Zealand disappeared tomorrow, the world would continue eating. Global commodity markets would adjust. But customers who value trusted supply, ethical production and dependable partners would notice.

The challenge is ensuring they still notice 25 years from now.